Understanding events at Liverpool

Understanding events at Liverpool 24 May 2012

It has been a fairly eventful couple of weeks at Liverpool and a number of pundits have expressed their surprise at how a manager that has reached two cup finals could be sacked. To understand the situation, a good place to start is with the club accounts.

Firstly, I should direct readers to Swiss Ramble's excellent blog where he covers Liverpool's finances in his usual superb manner. By using the club accounts, Swiss Ramble's analysis and my work on amortisation (below), we can come up with a potentially reasonable projection on the direction that the club are headed.

The attached projection is based on a number of assumptions that are outlined in the Notes section. The projection covers the season that has just finished and next season (2012/13). The projection takes a fairly flat assumption and also assumes that the club don't make any new player sales or purchases (of course this is very unlikely but it provides a useful starting position).

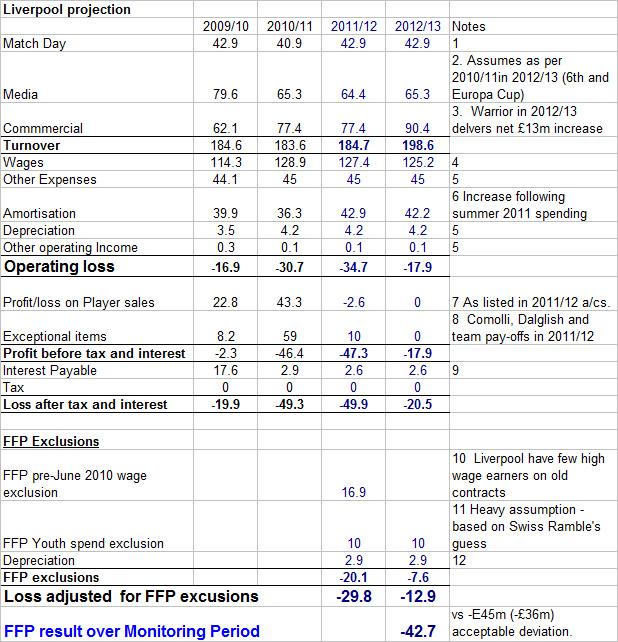

My projection looks like this:

Although the actual accounts for the season just finished won’t come out for another 11 months, we can work out what the accounts will probably say. A number of facts are now know (UK Media payments, Merit awards, transfers, and the main current sponsorship deals). However, as with all projections it carries a heavy 'health warning'.

All things being equal, Liverpool look as if they could just fail the FFP test in the first Monitoring Period with an aggregate loss for FFP purposes of around £42.7 (vs the permitted loss of £36m). This is pretty close and it perhaps wouldn't take much tweaking round the edges to get the club to pass the test. Worringly, without additional revenue, they might even fail future Monitoring Periods (during 2012/12, 2013/14 and 2014/15 average losses need to under £8m a season vs the -£12.9 figure for 2012/13 show above). However the projection does assume the club doesn't make a profit from player sales next season so there is certainly some scope for the club. If you aren't overly familiar with how the FFP rules work, please watch this 6 minute video.

Perhaps, just as worrying as the FFP results, the club look set to repeat the circa £50m loss reported for the previous season. The club is impacted by a number of factors in the 2011/12 season

- Significant Amortisation increase as a result of Summer 2011 signings

- A loss player sales (we already know this figure from the Post Balance Sheet events listed in the accounts)

- The pay-off for Comolli and Dalglish (listed as Exceptional events)

- Missing out on the Champions League (and the £25m - £50m revenue

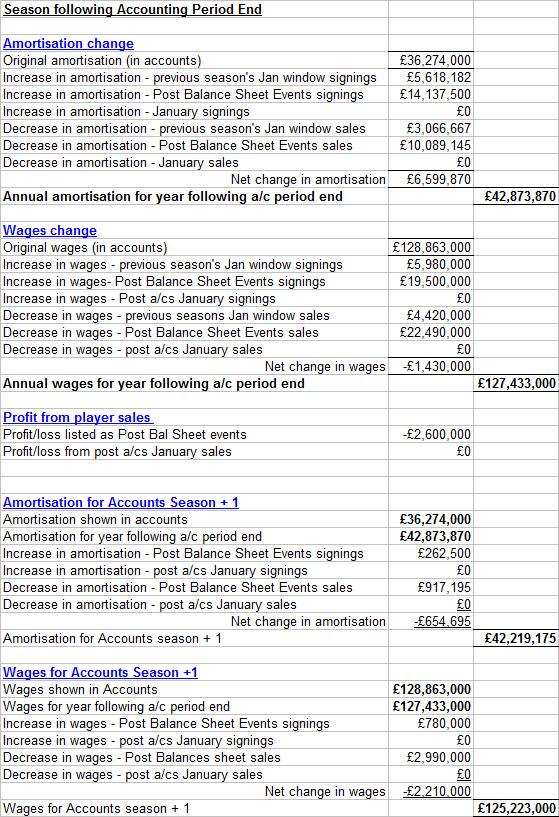

I covered Amortisation in a recent article on City and also in a video here. In summary, If a club goes out and buys a player for £20m on a 4 year deal, they will record only £5m in the accounts as an expense for that year ( £20m / 4). For the next three years they will also record an expense of £5m per year. The cost of buying the player is amortised or 'written-down' over the life of the contract - even if Liverpool pay cash upfront for the player, they have to record the expense on a phased basis. The figure for how much a club has paid out in Transfer fees appears as a note in the accounts detailing changes in 'intangible fixed assets' but there is never a specific line in the Profit and Loss Account section headed 'Transfer fees paid out' - the P&L only ever contains 'Amortisation'. Amortisation at Liverpool looks to have increased as a result of the last Summer’s heavy spending and the spending in the January 2011 transfer window (n.b. the profit from Torres appears in the 2010/11 accounts). My model indicates that amortisation has increased by around £6.6m a year. Liverpool will therefore have to live with the impact of Dalglish and Comolli’s expenditure for several years to come.

We also should not ignore FFP. Despite the owner’s wealth, Liverpool cannot afford to spend very heavily and be sure to pass FFP. To meet the FFP tests, Liverpool's new purchases need to be largely funded by player sales for above their book value (selling Downing, for example, for £10m would do little to help as his current book value is around £15m). This may well explain the difficulty the club is having in attracting a new manager. Looking at the accounts, some of the media stories, such as the rumoured appointment of Redknapp, with a guaranteed ‘war chest’ to spend on new players, seem to be out of touch with reality. The club will also not fancy paying-off the contract of a manager currently at a club with a long contract. Martinez with a limited budget (largely financed by player sales) looks much more likely.

The rumour of Dalglish turning down the ‘£8m pay-off’ was interesting. Although the rumour was discredited, the club can ill-afford this kind of hit (on top of the Comolli pay-off). These pay-off figures are shown in the accounts and in the above projection as Exceptional Items. The club were hit with a large Exceptional Item cost last year (2010/11) for the abortive plans for the new ground, plus the Hodgson pay-off.

Looking at the accounts, the club probably need a manager who can make the best with what, on paper at least, should be a decent squad. Dalglish wasn’t able to get the team to gel so it looks like the board will be looking for someone to get the best out of what is already there. The figures suggest that there won’t be a great deal in new funds for the new manager.

Another problem for the club is the fact that the major Commercial deals (sponsorship and kit) were signed comparatively recently and cannot be renegotiated for a few years. The 2010/11 accounts include the start of the Standard Chartered sponsorship and the Warrior deal kicks in next season (2012/13). Given the need to generate cash, the recent stories about the club negotiating Naming Rights for Anfield make a great deal of sense. Although possibly unpopular, this kind of deal would inject much-needed funds and give the new manager something to work with.

Under Comolli, the club gave a number of new contracts in the summer to players who were on old contracts (pre-June 2010). These can not now be excluded from the FFP test. As a result of contract extensions, and player turnover, Liverpool can’t fully take advantage of the exclusion rule which applies to the 2011/12 season only. Liverpool can only exclude around £16.9m in pre-June 2010 wages. As a comparison, Man City can exclude around £53m in wages for long-standing players, and at Chelsea the players that can be excluded appears to run into double-figures. This doesn't look like good planning by Comolli and the Liverpool board.

As Ian Ayre wrote in Directors’ Report section of the club accounts “football success is a key driver of commercial success”. Without the £25m+ from the Champions League the club can’t move forward. However the current squad is fairly weak and they may need to spend more money to achieve this. Unless the new manager can get the most out of the current squad, this looks like a Catch 22 situation for Liverpool.

Note: the FFP projection includes an exclusion for ‘expenditure on youth development activities’. Swiss Ramble assumed £10m a season for City as a marker – I have used this figure but have little idea if it is correct for Liverpool. It could make a big difference for the FFP test if the club could shoe-horn more expenditure under this category

Notes

The projection assumes the club finish 6th next season, do not win any of the domestic cups and do not progress much beyond the group stage of the Europa League.

1 Match Day (tickets)

Assumes ticket sales as at 2009/10 (when club reached group stage of Champions League).

2. Media

League TV and Merit payment amount for 2011/12 have been announced. In 2011/12, the club got to two finals but missed out on the E6.1m (£5m) in Europa League payments received in 2010/11). Europa League payments will be received again next season.

3 Commercial income

Commercial income increased in 2010/11 owing to the Standard Chartered deal commencing. In 2012/13, the club will receive a net increase of £13m a season from the Warrior deal (again, thanks to Swiss Ramble for figure).

4 Wages

Since last season's accounts (2010/11), the club have lost Kyriagos, Insua, N'Gog, Poulson, Miereles, Konchesky, Jovanovic, Torres (part season), Ince, Ayala and Mavinga, but gained Carroll (part season), Suarez (part season), Bellamy, Enrique, Downing, Adam, Henderson, Doni, Biyev and Ward. Wages are therefore fairly flat but increase slightly in 2012/13 - see 6 Amortisation for details.

5 Other Expenses

Flat assumption

6. Amortisation

I have calculated the amortisation and wage changes as follows:

7 Loss on Player sales

For 3 out of the past 4 seasons, Liverpool have made significant profits from selling players .

| 2007/8 | 2008/9 | 2009/10 | 2010/11 | ||

| Profit on player sales (£m) | 21.6 | 4.1 | 22.8 | 43.3 |

Since July 2011, the club have made a profit from player sales of £2.6m (relating to book-value 'profit' on Meireles and a loss on Konchesky). This figure is recorded in the accounts as a ‘post balance’ sheet event – i.e. a know fact that happened after July 2011. For this exercise, I will assume the club doesn’t sell any more players before the end of July 2012. I have also assumed it makes zero profit or loss from player sales for 2012/13 - this is an unlikely scenario but will help us to see what the club need to do to pass the FFP test

8 Exceptional Events

Estimated £2m pay-off for Comolli and £8m pay-off for Dalglish and assistant in 2011/12. Assumed the new manager does not need to bought out of contract and no Exceptional Events next season.

9 Interest

Liverpool has £38m of bank loans (plus £30m other non-interest paying debt to the holding company). I have assumed an interest rate of 7% (or £2.3m a year) on the £38m bank debt.

10 Players signed before 1 June 2010

The wages for any players on contracts signed before 1 June 2010 are excluded from the FFP test for the 2011/12 season only. Re-negotiated contracts cannot be excluded. For Liverpool, this probably amounts to around £16.9m for the following players:

| £k pw | £m | ||||

| Gerrard (half season) | 120 | 3.12 | |||

| Agger | 90 | 4.68 | |||

| Rodriguez | 90 | 4.68 | |||

| Jonjo Shelvey | 25 | 1.3 | |||

| Sterling | 25 | 1.3 | |||

| Suso | 20 | 1.04 | |||

| Gulacsi | 15 | 0.78 | |||

| 16.9 | |||||

Note. It is quite possible that Gerrard's wages for part of the season may not be an excludable item as he signed a new contract part way through the season - the FFP rules are not entirely clear in this area.

11 Other FFP exclusions

Clubs can exclude any spend on Youth player development from the FFP test - it is hard to extract this information from the accounts but I have used the same £10m marker as Swiss Ramble assumed for City

12 Depreciation

FFP rules allow Depreciation of Fixed Assets to be excluded from the FFP test.

blog comments powered by Disqus